Operationalizing Financial Services AI

- Rajesh Koppula

- Jun 10

- 22 min read

From AI Gloss to Multi-Agent Reality — An Executive Blueprint

The board conversation around AI has crossed a threshold. The era of the single-prompt chatbot and the isolated proof-of-concept is over. Boards are no longer tolerating activity metrics and slide-deck pilots. They are demanding a line on the operating margin.

The frontier of financial services is no longer about automation. It is about Agentic AI — networks of specialized agents that can reason, plan, and autonomously execute complex, multi-step banking workflows end-to-end. The institutions winning this race are not those who deployed the most AI tools. They are the ones who redesigned their operating models around them.

But here is the structural danger hiding inside most roadmaps: deploying an AI agent on top of a broken workflow does not fix the workflow. It produces broken results ten times faster. True transformation demands an operational blueprint that marries cutting-edge intelligence with ironclad governance — from the first line of code to the board pack.

1. Ten Live Deployments Worth Studying

To understand where the market is moving, look past the announcements and into production environments.

JPMorgan Chase (LLM Suite + COiN): JPMorgan now runs over 450 AI use cases in production — targeting 1,000 by 2026 — against an $18 billion annual technology budget. The LLM Suite serves over 200,000 employees, the largest Wall Street AI deployment, while COiN (Contract Intelligence) saves 360,000 work hours annually by processing 12,000 commercial credit agreements. JPMorgan employees using the internal LLM report saving four hours per day from the technology.

Morgan Stanley (AskResearchGPT + Agent Funnel): A platform that parses the firm's entire proprietary research library for instant, compliant wealth management answers. Morgan Stanley is now opening its wealth management platforms directly to external AI agents, allowing clients' autonomous systems to pull data from equity administration platforms — one of the earliest instances of a major Wall Street bank opening its infrastructure to external AI tools.

American Express (Real-Time Fraud Engine): Evaluates over $1.2 trillion in annual transactions, processing multi-variable fraud vectors in milliseconds at point-of-sale — a system that has been in continuous production learning for over a decade and sets the benchmark for behavioral streaming in card payments.

Capital One (MACAW): An internal multi-agent orchestration architecture designed to handle complex, multi-step customer journeys — from auto-financing math to personalized savings strategies — without human handoffs at each stage.

Commonwealth Bank of Australia (Project Coral): An autonomous multi-agent system deployed directly within engineering to optimize codebase maintenance and accelerate software delivery cycles — a model for how infrastructure teams can absorb AI natively rather than bolting it on.

Goldman Sachs (Legacy Code Modernization): Utilizing generative models to ingest decades-old COBOL mainframe code, map its underlying business logic, and autonomously refactor it into modern Python and Java — addressing a technical debt problem that would take engineering teams decades to resolve manually.

Westpac (Kai-GPT): Leveraging Domain-Specific Language Models trained natively on hyper-curated, proprietary banking data — bypassing the hallucination risks of general-purpose models entirely. One of the clearest early proofs that purpose-built beats general-purpose in regulated pipelines.

Klarna (AI Support Agent): The most publicly documented AI deployment in fintech. Klarna's AI agent now does the equivalent work of 853 full-time agents — up from 700 at launch — and the CEO credits it with saving $60 million. Customer service costs per transaction dropped 40% over two years, from $0.32 to $0.19. Critically, Klarna's story carries a second chapter worth understanding: by mid-2025 they reintroduced human agents for complex and emotionally charged cases, validating what practitioners already know — AI scales tier-one support brilliantly, but human judgment remains the essential backstop for nuanced resolution. That is not a failure. That is the model.

BlackRock (Aladdin AI): Integrating generative language interfaces into its legendary risk platform, allowing institutional asset managers to query massive multi-asset portfolios using plain language — and closing the gap between quantitative insight and executive decision-making speed.

Lemonade (AI Jim & AI Maya): Fully operational AI workflows that onboard customers, calculate risk pricing, and automatically settle straightforward property claims in under three seconds without human intervention — the clearest proof point that end-to-end agentic insurance processing is not a future-state concept.

2. The Market Reality: What the Scorecards Actually Show

Read across corporate earnings and C-suite communications and the narrative splits cleanly into two realities.

The Technical Wins: Engineering and support organizations are outperforming. AI-assisted developer copilots are delivering coding cycle time reductions of 30% or more. Customer support operations are absorbing massive scale increases without proportional headcount additions. The firms moving fastest are not the ones with the largest AI budgets — they are the ones with the clearest operational accountability chains behind their deployments.

The CFO's Measurement Gap: Despite heavy board pressure, precisely calculating ROI on AI investments remains genuinely difficult. Fewer than 10% of financial institutions can cleanly isolate AI-related costs against precise revenue yields. The honest answer is that most value right now is not appearing as new revenue. It is buried in the operating margin — faster onboarding, lower fraud losses, reduced compliance friction, and compressed support costs.

The firms building durable moats understand this distinction. They are not chasing AI headlines. They are engineering structural efficiency gains that compound quarter over quarter — and they are building the measurement infrastructure to prove it to their boards before their competitors do.

3. Operationalizing the Verticals: Where Control Points Define the Outcome

Moving past superficial adoption requires understanding how multi-agent frameworks map to the specific plumbing of each vertical. A generic algorithm is not an answer. The answer is a precisely defined accountability chain — where the human sits, what decision they own, and how quickly they must act. In regulated environments, the control architecture is not optional. It is the product.

a) Credit Cards — Behavioral Streaming & Real-Time Optimization

Modern card platforms ingest hundreds of dynamic variables simultaneously — biometric typing velocities, location telemetry, micro-merchant categories — running machine learning models in milliseconds at point-of-sale. Beyond fraud, these engines power real-time limit optimization and adaptive rewards structures that analyze a consumer's purchasing path before the transaction clears.

Control Points: Pre-decision, risk teams set macro velocity and geographic risk tiers rather than reviewing individual swipes. Post-decision, data scientists asynchronously tune model feature weights against emerging fraud ring patterns on a weekly cycle. Exception handling routes false positives to instant step-up authentication — a biometric challenge in the banking app — without killing the transaction at the counter.

b) Payments & Transaction Processing — Provenance Over Precision

High-volume cross-border flows have historically generated settlement breaks consuming days of manual triage. Deep anomaly detection models now surface real exceptions in minutes. But the operational stress test is not speed — it is defensibility.

If your model flags a settlement break and your operations team cannot reconstruct the exact logic trail six months later for an auditor, you have not automated a control. You have automated a liability.

At Katalyst Street, this is a foundational design principle behind DeltaMax: provenance must outrank precision. True explainability requires dissecting each transaction across business rules, data drift, and data freshness signals simultaneously — and weighting them dynamically to produce a fully auditable, defensible compliance narrative that survives regulatory scrutiny.

Control Points: Pre-decision, treasury operations define FX margin tolerance bands for straight-through routing. Post-decision, audit teams review daily automated samples of matched settlement pairs against compliance trails. Exception handling surfaces a centralized Trust Score breakdown on high-value anomalies before market close, giving operators a full narrative — not just a flag.

c) Crypto & Digital Assets — Smart Contract Governance & Cross-Chain AML

Multi-agent systems now execute continuous autonomous smart contract audits before institutional liquidity injections. AI token-tracking networks map cross-chain capital flows in real time, identifying wash-trading patterns, liquidity pool exploits, and illicit mixers before decentralized assets interface with traditional fiat ledgers.

Control Points: Pre-decision, asset managers define blacklisted wallet clusters and code-vulnerability severity limits within the automated scanner. Post-decision, compliance engineers monitor historical cross-chain pathing maps to train defensive models against shifting mixer algorithms. Exception handling freezes flagged transactions and pulls a cryptographic lineage audit report to justify the hold before it can be challenged legally.

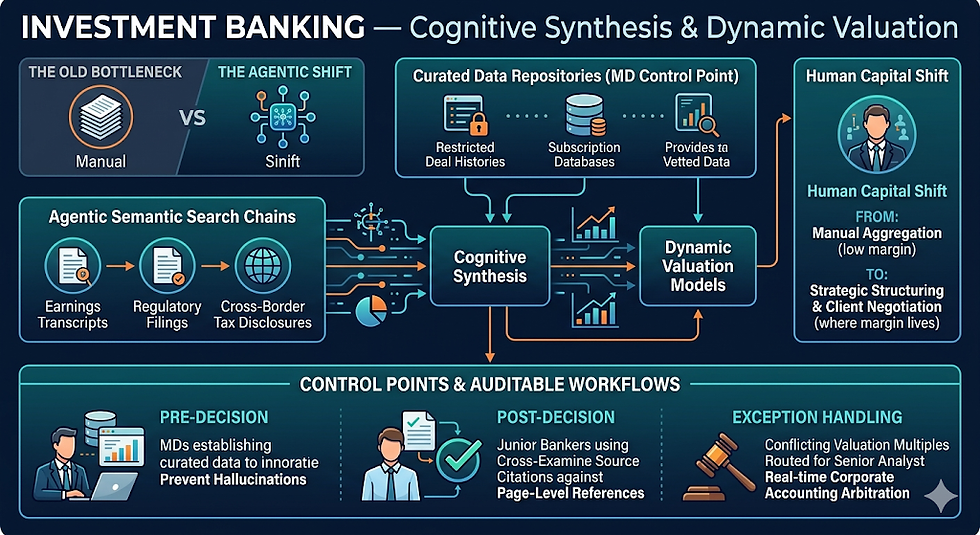

d) Investment Banking — Cognitive Synthesis & Dynamic Valuation

The IB operational bottleneck has always been data ingestion. Agentic semantic search chains now ingest and synthesize hundreds of earnings transcripts, regulatory filings, and cross-border tax disclosures in the time it previously took an analyst team an entire night. The human capital shift is significant: from manual aggregation to strategic structuring and client negotiation — which is where the margin actually lives.

Control Points: Pre-decision, managing directors establish curated, vetted data repositories — restricted deal histories and subscription databases — to prevent agents from citing hallucinated public data. Post-decision, junior bankers cross-examine source citations against auditable page-level references. Exception handling routes conflicting valuation multiples across legal entities to a senior analyst for real-time corporate accounting arbitration.

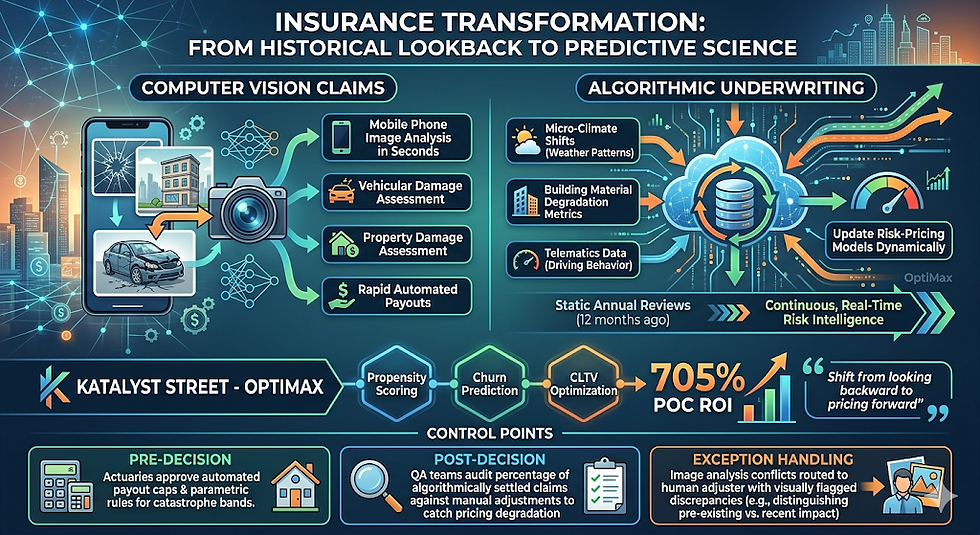

e) Insurance — Computer Vision Claims & Algorithmic Underwriting

Carriers are transforming the actuarial function from historical lookback to predictive science. Computer vision models assess property and vehicular damage from mobile phone images in seconds. Generative models cross-reference micro-climate shifts, building material degradation metrics, and telematics data to update risk-pricing models dynamically — enabling underwriting that tracks real-world risk as it evolves rather than as it was twelve months ago.

At Katalyst Street, OptiMax directly addresses this transformation — deploying propensity scoring, churn prediction, and CLTV optimization models that allow carriers to shift from static annual pricing reviews to continuous, real-time risk intelligence. The 705% POC ROI narrative we have documented with insurance clients reflects exactly this architectural shift: from looking backward to pricing forward.

Control Points: Pre-decision, actuaries approve automated payout caps and parametric rules for catastrophe bands. Post-decision, QA teams audit a percentage of algorithmically settled claims against manual adjustments to catch pricing degradation before it becomes a portfolio problem. Exception handling routes image analysis conflicts — distinguishing pre-existing damage from recent impact — to a human adjuster with discrepancies visually flagged.

f) Lending & Brokerage — Alternative Data & Margin Optimization

Traditional credit scoring locks out thin-file borrowers structurally. Modern platforms bypass this by ingesting alternative data ecosystems — utility cash flows, digital payment velocities, trade inventory cycles — to calculate probability-of-default scores in minutes. The addressable lending market expands safely while portfolio margins are optimized dynamically across the full credit cycle.

Control Points: Pre-decision, credit risk officers define allowed alternative data inputs and macroeconomic stress-test limits for the pricing engine. Post-decision, portfolio managers run continuous vintage cohort analysis to catch credit drift early across alternative data segments. Exception handling introduces qualitative override inputs — relationship history, local market tenure — when algorithmic flags hit borderline corporate applications.

g) Retail Banking — Multi-Agent Self-Service at Scale

Today's retail agentic networks are not chat widgets. They have read-write access to core banking systems. They resolve disputed transactions, calculate mortgage pre-qualification math, and guide customers through complex account-merging procedures — absorbing upward of 40% of tier-one operational volumes without human escalation.

Control Points: Pre-decision, product and legal teams establish conversational guardrails, data-privacy anonymization filters, and maximum automated refund authority limits. Post-decision, support supervisors asynchronously sample transcript clusters via sentiment analysis to detect logic loops or agentic drift before it reaches customers. Exception handling seamlessly transfers the full chat state, account history, and intent roadmap to a live banker when distress signals appear — with zero restart friction for the customer.

h) Venture Capital & Private Equity — Sourcing Intelligence & Portfolio Health

Leading firms construct proprietary data-ingestion pipelines monitoring millions of digital signals simultaneously — developer hiring velocities, software package downloads, localized web traffic shifts — to surface off-market acquisition targets months before formal banking processes begin. Post-acquisition, the same engines run automated operational health scorecards to detect and remediate customer churn anomalies across portfolio brands.

Control Points: Pre-decision, investment committees define vertical parameters, growth metric thresholds, and geographic constraints for sourcing filters. Post-decision, associates validate data freshness to ensure pipeline targets are not built on decayed metrics. Exception handling flags internal duplicate anomalies — targets that could mask competition with an active portfolio brand — for deep deal-clearing analysis before any capital is committed.

4. The Global Regulatory Split: Twelve Philosophies, One Architecture Problem

The governance conversation has moved past vague ethics guidelines and into hard operational compliance mandates. Multinational institutions must now design AI architectures that simultaneously satisfy five distinct regulatory philosophies — and for organizations operating across geographies, that design constraint is itself a strategic variable.

The US: Voluntary Frameworks With De Facto Enforcement. Early 2025 brought a decisive federal turn toward deregulation, with executive orders revoking earlier safety-focused guidance and directing agencies to prioritize innovation and economic competitiveness over precautionary oversight. In the absence of a federal standard, states including California, Colorado, and Texas have pursued their own AI transparency and consumer protection frameworks, creating a patchwork that multinationals must navigate carefully. CISA and NSA benchmarking standards for frontier models touching critical financial infrastructure still function as de facto requirements for clearing systemic risk audits — regardless of formal mandate status. Americas QuarterlyLatin Counsel

The EU: Prescriptive Hard Law. The EU AI Act drives mandatory independent audits, strict log data requirements, and rigid real-time human override capabilities for any model touching credit scoring or payment risk assessment. Compliance is not optional; it is a precondition for market access. Europe's forthcoming Cloud and AI Development Act (CAIDA) is expected to institutionalize data sovereignty requirements further, meaning institutions operating in the EU must plan not just for current obligations but for a tightening regulatory floor. The architectural implication: EU-facing AI systems need explainability baked in at the model level, not bolted on at the reporting layer. Americas Quarterly

India: Innovation Over Restraint via Digital Public Infrastructure. On August 13, 2025, the RBI released the FREE-AI Framework — Framework for Responsible and Ethical Enablement of Artificial Intelligence — a significant milestone in structured AI governance across banking, financial services, and insurance. Built on seven guiding principles (Sutras) and 26 recommendations across six strategic pillars, it applies to all RBI-regulated entities including commercial banks, NBFCs, payment system operators, and fintechs. India's approach is architecturally distinct: it embeds AI governance directly into its world-class Digital Public Infrastructure rails — including the Unified Lending Interface — enabling alternative data scoring models that use satellite land imagery, agricultural production metrics, and regional cash flows to extend credit to millions without traditional credit histories. The RBI's "Banking BHASHINI" initiative extends this further: a domain-specific small language model built on banking vocabulary across India's diverse linguistic landscape, designed to scale conversational banking while enforcing native real-time AML monitoring. The Legal 500Regulations

APAC: Tiered Pragmatism Led by Singapore. In November 2025, the Monetary Authority of Singapore released its Consultation Paper on Guidelines on Artificial Intelligence Risk Management — a lifecycle AI risk management framework that differentiates governance requirements by risk level rather than applying uniform rules across all systems. Built on FEAT principles — Fairness, Ethics, Accountability, Transparency — the guidelines require board-level AI oversight, three lines of defense, and a comprehensive AI inventory across all MAS-regulated institutions, including banks, insurers, fintechs, and payment providers. Critically, third-party AI tools are covered: institutions cannot delegate governance obligations to vendors. Singapore's framework is setting the tone for the broader APAC region. The common thread across Singapore, Malaysia, Australia, and New Zealand is proportionality: governance intensity scales with risk impact on customer outcomes, not with model size or vendor pedigree. It is the most operationally pragmatic of the five frameworks — and for institutions building globally, it offers a useful design reference. HankunlawPertama Partners

LATAM: Brazil Leads, Region Follows. Brazil is the first Latin American nation to formalize AI governance, with its AI Bill (No. 2338/2023) passed in the Senate in December 2024 and advancing toward full enforcement in 2026. The legislation is centered on fundamental rights protection and preventing AI-driven discrimination — philosophically close to the EU approach but calibrated for Brazil's fintech-forward environment. Most other Latin American countries — Chile, Mexico, Argentina, and Colombia — are in early stages of drafting national AI strategies but have not yet enacted binding laws, meaning the effective compliance floor for most of the region is still existing data protection legislation. A regional multi-country initiative has announced Latam-GPT, a public-interest LLM tailored to regional languages including indigenous ones — a signal of where regulatory procurement baselines are heading. For multinationals, the near-term LATAM posture is clear: build to Brazil's standard and you will have covered most of what the region will eventually require. Xenoss + 2

EMEA: Three Distinct Regulatory Cultures Within One Region

EMEA is not a single regulatory philosophy — it is three fundamentally different postures operating under one geographic label. Treating the region as homogenous is one of the most common and costly mistakes multinationals make when designing their AI governance architecture.

United Kingdom: Principles-Based, Outcomes-Focused, Deliberately Flexible. The UK has made a deliberate strategic choice to diverge from the EU's prescriptive model post-Brexit. In December 2025, FCA Chief Executive Nikhil Rathi reaffirmed that the regulator will not introduce AI-specific rules, citing the technology's rapid evolution every three to six months. Instead, the FCA is doubling down on its principles-based, outcomes-focused approach — committing to intervene only in cases of egregious failures not addressed by firms themselves. This is not regulatory passivity. The FCA, PRA, and Bank of England are investing heavily in sandbox initiatives and long-term reviews to test whether existing frameworks remain fit for purpose as AI deployment accelerates. The first cohort of firms joined AI Live Testing in October 2025, with a second cohort expected in April 2026. A Bank of England and FCA survey found 75% of UK financial firms already using AI, with 59% now reporting measurable productivity gains — up from 32% a year earlier. The UK's bet is that adaptive oversight and sandbox-led learning will allow it to move faster than jurisdictions locked into hard law — and that the FCA's strategic partnership with Singapore's MAS gives it a global read on where outcomes-based AI governance is proving durable. The Legal 500 + 2

Middle East: UAE as the Region's AI Ambition Standard-Bearer. The UAE has positioned itself as the most proactive AI governance environment in the Middle East, operating through a layered architecture of federal law and free zone frameworks. DIFC Regulation 10, in force since January 2026, requires AI impact assessments, transparency obligations for AI-driven decisions, and documentation of high-risk AI use cases — with fines of USD $25,000–$50,000 per violation. The DIFC Data Protection Law 2020, amended in 2025, mirrors GDPR with a private right of action for data subjects. At the market level, AI adoption in the DIFC nearly tripled over the prior year, though governance practices are still maturing — with regulatory uncertainty remaining the primary concern for firms operating in the zone, and firms actively calling for clearer guidance on AI oversight, ethical use, and accountability. Saudi Arabia is moving in parallel: under Vision 2030, Microsoft has committed to a new cloud data center region in the Kingdom — planned to be operational in 2026 — specifically to support sovereign AI deployment and data residency requirements for government and regulated industries. The GCC pattern is clear: states are investing in sovereign AI infrastructure first, with regulatory frameworks following behind the capital. Institutions entering the Gulf should expect the governance floor to rise rapidly as infrastructure matures. Twig + 2

Africa: Fragmented Today, Converging Fast. Africa's AI regulatory landscape is the most heterogeneous of the three EMEA sub-regions — and also the one moving fastest from a financial inclusion standpoint, which makes governance design here uniquely consequential. About a quarter of emerging market and developing economy financial authorities now have formal AI governance policies, though only one-fifth of African authorities have reached that threshold — with most expecting to establish formal strategies by mid-2026. South Africa is the most advanced: at the end of 2025, the Financial Sector Conduct Authority and Prudential Authority published a joint survey on AI in the South African financial sector, with a formal AI regulatory framework and ethical use guidelines expected to follow in 2026. Nigeria is moving on a parallel track: the Central Bank of Nigeria's 2025 Fintech Report named AI as a priority regulatory focus area, and 87.5% of Nigerian fintechs now deploy AI primarily for fraud detection — the most widely deployed AI application in the sector. Kenya sits at the intersection of mobile financial infrastructure and AI credit innovation: firms are leveraging AI to parse structured and unstructured financial data in real time, extending credit to thin-file borrowers at scale — with the CBK requiring AI-driven credit decisions to be explainable on request under its Digital Credit Providers Regulations. In Ethiopia, more than 380,000 MSMEs accessed USD $150 million in uncollateralized credit facilities driven by AI credit scoring — one of the clearest proof points on the continent that AI-enabled financial inclusion is not aspirational. It is operational. On Point + 4

The Africa signal for multinational institutions is the same one that defined mobile payments a decade ago: the infrastructure constraints that force innovation here are producing governance models built natively for low-data, high-volume, high-inclusion contexts that advanced markets are now trying to retrofit into their own systems.

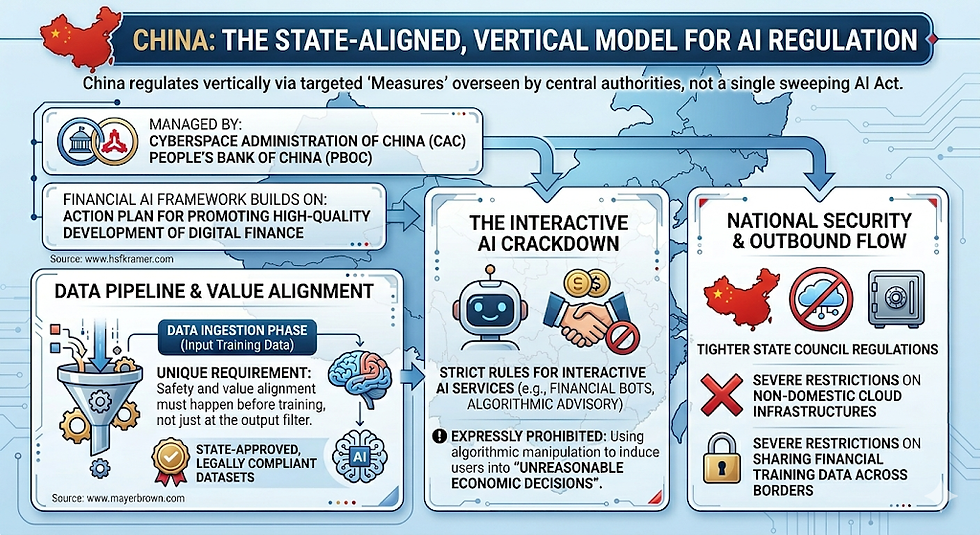

China: The State-Aligned, Vertical Model

China does not use a single, sweeping AI Act. Instead, Beijing regulates vertically via targeted "Measures" managed by the Cyberspace Administration of China (CAC) and the People’s Bank of China (PBOC). For financial services, the regulatory framework builds heavily on the Action Plan for Promoting High-Quality Development of Digital Finance. www.hsfkramer.com+ 1

Data Pipeline & Value Alignment: China is unique in requiring safety and value alignment at the data ingestion phase, not just the output filter. Financial institutions must train models using state-approved, legally compliant datasets.

The Interactive AI Crackdown: Under strict rules for interactive AI services, financial bots and algorithmic advisory systems are expressly prohibited from using algorithmic manipulation to induce users into "unreasonable economic decisions."

National Security & Outbound Flow: With the State Council's tighter regulations on outbound investments and data transfers, Chinese financial entities face severe restrictions when utilizing non-domestic cloud infrastructures or sharing financial training data across borders.

Japan: The "World's Most Friendly" AI Runway

Japan has explicitly positioned itself to become the world’s most permissible environment for developing and utilizing AI, firmly rejecting the EU's heavy fine-based structures. Following its foundational AI Act, Japan's approach relies heavily on agile governance. www.whitecase.com

FSA Iterative Guidance: The Financial Services Agency (FSA) actively collaborates with the private sector through its AI Discussion Paper series to co-create risk management frameworks rather than issuing rigid mandates. mofotech.mofo.com

The Major Data Loophole: Japan's landmark revisions to the Act on the Protection of Personal Information (APPI) established a "statistical processing" exception. Financial institutions can legally train AI models on consumer data without prior user consent, provided the data is stripped of identifying details (pseudonymized) and used strictly for AI or statistical research. blog.gaijinpot.com

The Guardrail: To balance this massive data runway, Japan enforces harsh, profit-proportional fines if a financial firm experiences large-scale data misuse or attempts to contractually re-identify individuals. blog.gaijinpot.com

Hong Kong: The Pragmatic Financial Hub

As a global financial nexus, Hong Kong walks a fine line: maintaining compatibility with Beijing's overarching data-sovereignty principles while remaining open to western open-source models. The Securities and Futures Commission (SFC) and Hong Kong Monetary Authority (HKMA) favor a highly accountable, principles-based framework.

Massive Enterprise Adoption: GenAI has evolved rapidly from pilot to operational reality, with recent data showing roughly 75% of banks, wealth managers, and insurers operating live GenAI use cases. mco.mycomplianceoffice.com

Strict Third-Party/Open-Source Liability: The SFC explicitly warns that using open-source models (like Meta's Llama) or third-party enterprise providers does not absolve financial institutions of regulatory liability. Intermediaries must prove continuous model due diligence.

Human-in-the-Loop Mandates: Regulations demand clear documentation, bias mitigation, and human oversight. If an automated credit-scoring or trading model fails, accountability lands squarely on the firm's board and licensed executives.

Russia: The Anti-Overregulation Stance

Faced with international sanctions and a pressing need to catch up to US and Chinese AI capabilities, Russia’s regulatory regime for the financial sector is intentionally hands-off.

Fear of "Overregulation": Central Bank of Russia (CBR) leadership and executives from major state banks (such as VTB and Alfa-Bank) have openly stated that detailed, restrictive legislation would cause the domestic financial market to stagnate. interfax.com

The Soft Code of Ethics: The CBR relies almost entirely on an advisory Code of Ethics for AI in Finance. It emphasizes basic principles: informing clients when they are interacting with an AI, offering human-takeover alternatives, and respecting personal data confidentiality.

The Leapfrog Strategy: While the Ministry of Digital Development continues to work on a foundational AI bill slated for late 2027, the current legislative focus remains focused on stimulating domestic sovereign models rather than restricting algorithmic deployment.

The Architecture Implication Across All Twelve. No single governance architecture satisfies all five regimes simultaneously without intentional design. Explainability requirements vary. Data residency rules diverge. Human override mandates differ in scope and timing. The pragmatic answer for institutions operating across geographies is a modular governance layer — compliance behavior that is configurable by jurisdiction — rather than building to the most restrictive global standard and accepting the operational drag everywhere else. That modularity is an architectural decision, and it needs to be made before the models are built, not after they are in production.

5. The Threat Paradigm: When Exploitation Speed Outpaces Defense Architecture

While financial institutions turn AI inward to optimize operations, the external threat landscape has shifted in a way that invalidates traditional security assumptions — and the market is responding with significant capital consolidation.

The Core Problem: The Exploitation Window Has Collapsed. Historically, the interval between vulnerability discovery and a working exploit gave enterprise patch teams a manageable buffer — weeks to months. That buffer no longer exists. According to Palo Alto Networks' Unit 42 2026 Threat Intelligence Report, attackers now scan for vulnerabilities and initiate exploitation within 15 minutes of a CVE disclosure. Once inside a network, adversaries achieve initial access to full data exfiltration in an average of 4.2 hours — four times faster than 2023. The gap between when a flaw is found and when it becomes an active production threat is now measured in hours, not planning cycles. Everything PR

Identity-based attacks dominated the 2025–2026 threat landscape, with 90% of successful breaches involving compromised credentials or identity systems rather than traditional malware — with AI increasingly being used to conduct phishing, social engineering, and credential compromise at scale. Everything PR

For financial institutions specifically — which run on layered legacy dependencies, aging payment APIs, and complex clearing infrastructure — this matters acutely.

Systems that survived decades of manual security review did so because the review cadence was human-paced. That protection is now structurally insufficient.

The Vendor Response: Infrastructure Consolidation Around AI-Native Security. The market has responded with rapid consolidation around AI-native security platforms. Google acquired security platform Wiz for $32 billion and struck a roughly $10 billion multiyear partnership with Palo Alto Networks — the largest security services pact of its kind — specifically to build AI-driven enterprise security capabilities as corporate demand for automated threat detection accelerates. Yahoo Finance

The combined Google Cloud–Wiz platform provides continuous discovery and risk analysis across traditional and AI applications, including AI agents, models, and MCP servers, with AI threat protection covering both threats to models and threats originating from models. Google Cloud

Palo Alto's framing of the agentic threat is precise: once an AI agent can execute code, call APIs, and initiate financial processes without human oversight, it is no longer a chatbot — it is a privileged insider whose behavior can no longer be governed by the perimeter and identity controls that protected user-driven applications. Its Prisma AIRS platform now delivers unified visibility into agent traffic, runtime threat detection against agent-specific attack patterns, and automated routing controls across the enterprise. A 2026 Vorlon survey found that one in three enterprises experienced a confirmed or suspected security incident involving AI agents in 2025. Tech TimesTech Times

The Defender's Posture Shift. The CISO response architecture must evolve from static perimeter defense to automated continuous validation embedded directly in the development pipeline. The same class of AI capability accelerating external threats is the tool that makes enterprise defense viable at scale and speed. Codebases, middleware, and third-party SaaS integrations must be continuously interrogated by internal defensive AI models within the CI/CD pipeline — finding and hardening flaws before external actors reach them. The institutions treating this as a future-state initiative will learn the lesson expensively.

6. Three Trends Shaping the Next 24 Months

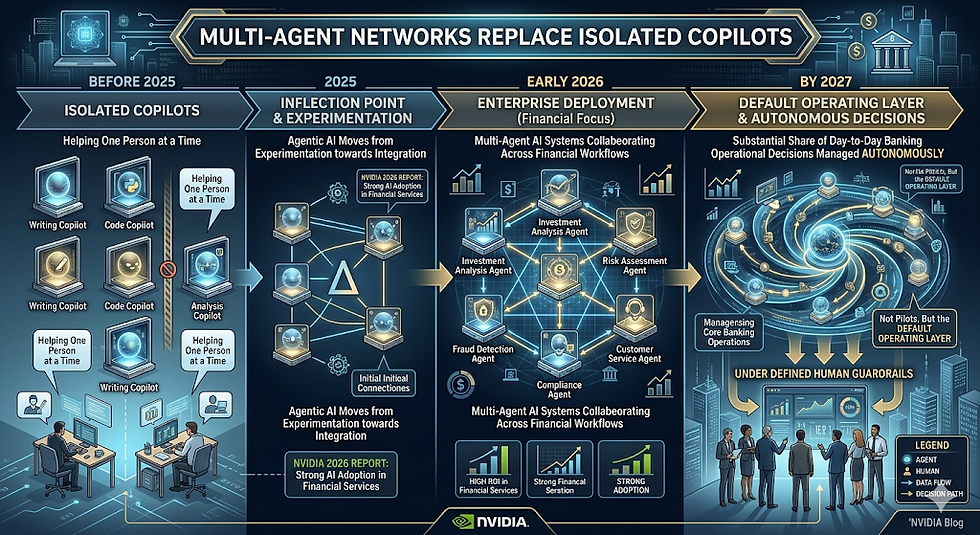

Multi-Agent Networks Replace Isolated Copilots. The evolution from single-model assistants to autonomous agent networks collaborating across workflows is past the inflection point. NVIDIA's 2026 State of AI report found that financial services showed among the strongest AI adoption and ROI results of any industry, with agentic AI moving from experimentation in 2025 to full-fledged enterprise deployment in early 2026. By 2027, a substantial share of day-to-day banking operational decisions will be managed autonomously by multi-agent systems under defined human guardrails — not as pilots, but as the default operating layer. NVIDIA Blog

Domain-Specific Language Models Displace General LLMs in Critical Pipelines. General-purpose models are being retired from production environments where precision, auditability, and regulatory defensibility matter. The replacement architecture is the Domain-Specific Language Model (DSLM) — a smaller, purpose-built model trained on clean, heavily curated institutional data that understands the difference between "margin" in finance and "margin" in retail, between "agent" in insurance and "agent" in AI.

The build-vs-fine-tune question has a practical answer for most institutions. The standard enterprise approach is fine-tuning an open-source foundation model — Mistral, LLaMA, Qwen, or Gemma — on proprietary domain data using parameter-efficient methods like LoRA. FinGPT, for example, achieved competitive financial sentiment analysis performance at roughly $300 per training run, compared to BloombergGPT's $2.7 million ground-up build cost. Building from scratch remains viable for institutions with proprietary data moats large enough to justify the investment, but it is no longer the default path. For most regulated institutions, fine-tuning a pretrained small model — Microsoft Phi-3, Google Gemma, Mistral 7B, or Meta LLaMA — on domain-specific institutional data represents the faster, more cost-efficient path to production, with models in the 7–13B parameter range routinely outperforming much larger general models on specialized financial tasks after targeted fine-tuning. Prem AIInfosys

Early production wins in financial services DSLMs illustrate the pattern: BloombergGPT for market data analysis and financial NLP; FinGPT for open-source financial sentiment and forecasting; Westpac's Kai-GPT for banking-native conversational AI; the RBI's Banking BHASHINI for multilingual compliance and customer banking. The common thread across all of them is access to curated, proprietary data that general models cannot reach — and each outperforms frontier general models on its specific domain task precisely because of that data advantage.

On-Premise and Sovereign AI Infrastructure: NVIDIA as the Enabling Layer. The regulatory and data sovereignty pressures described above — particularly in the EU, India, and APAC — are creating a structural pull toward on-premise and private cloud AI deployment. Sending sensitive customer data to a third-party cloud inference endpoint is not viable in jurisdictions with strict data residency requirements, and it is increasingly untenable from a competitive intelligence standpoint regardless of jurisdiction.

At GTC Paris 2025, one of Europe's largest financial institutions announced it is building an NVIDIA-powered AI factory to deploy sovereign AI across its financial services operations. NVIDIA's positioning here is deliberate: the company describes itself as the only platform that runs in every cloud, powers every frontier and open-source model, and scales from hyperscale data centers to the edge — and has restructured its reporting to reflect this with a new Edge Computing category specifically covering agentic and physical AI deployment at the institutional level. NVIDIA's RAPIDS Accelerator for Apache Spark delivers data processing acceleration of up to 5x and cost reductions of up to 4x for financial institutions running fraud detection and transaction analysis workloads on-premise. NVIDIA + 2

For institutions that need model inference latency measured in milliseconds — payment fraud, real-time credit decisions, AML monitoring at transaction speed — on-premise NVIDIA infrastructure is increasingly the architecture of choice, not a compromise. The practical design implication: build for a hybrid inference posture from day one. Cloud for development and latency-tolerant workloads; on-premise NVIDIA infrastructure for regulated, latency-critical, and data-sovereign pipelines. Institutions that defer this architectural decision will find themselves rebuilding around it later at significantly higher cost.

7. The Boardroom Test

When an AI roadmap hits the board pack, operators read it for efficiency gains and activity metrics. Directors must read it for judgment — and interrogate the foundational assumptions.The gap between those two reads is where most AI programs fail.

As outlined in Katalyst Street's Executive Framework for AI-Era Program Management, executing a real AI transformation requires multi-layered governance architecture built before deployment starts — explicit accountability vectors, data tokenization protocols, and defined kill-switches that exist before the first agent goes live. The board's role is not to approve the technology. It is to approve the operating model change that the technology demands.

Before approving the next AI initiative, ask three questions that open the room:

"Tell me what changed." Not what tools were added. What actually changed in the underlying business model? True transformation means building an Intelligence Layer that redefines the competitive moat — not layering software on top of an old operating architecture and calling it AI strategy.

"What are we not seeing here?" Activity metrics often mask ballooning compute costs, hidden technical debt, and the deepest friction of all: the human capital challenge of getting traditional teams to genuinely adopt and trust autonomous systems. That adoption gap is where most AI investments stall — and it rarely appears in a board pack.

"What would have to be true for this to be the wrong answer?" The wrong answer is assuming automation is the final destination and that humans are progressively eliminated from the loop. The actual frontier is Human Judgment + AI Automation — and designing the handoff architecture between them is the hardest, highest-value work in the entire program. The institutions getting this right are not automating people out. They are repositioning human capital toward the decisions that actually require it.

The Boardroom Test: If your board pack displays dozens of AI initiatives without clear executive ownership, explicit control points, human adoption friction plans, defined exception paths, and explicit measures of decision quality — the room is approving activity, not transformation.

The winning question is never "What can AI do?" It is "What has to change in our operating model for the answer to matter?"